How Does Student Loan Debt Impact Mortgage Approval?

Student loans can shape your financial profile when applying for a mortgage, but they don’t have to stand in the way of homeownership. Like other forms of debt, such as credit cards or car loans, student loans affect key metrics that lenders evaluate. By understanding how student loans influence mortgage approval, you can take steps to improve your chances of qualifying. Here’s what you need to know and how Ideal Credit Union can help.

Do Student Loans Affect Mortgage Approval?

When applying for a mortgage, lenders assess your debt-to-income ratio (DTI), credit score and overall financial health. While student loans are factored into these calculations, they are not inherently more restrictive than other types of debt. Lenders generally focus on:

- Monthly Payments: The amount you pay each month is what matters most, rather than the total balance of your loans. If your student loans are in deferment or forbearance, lenders may use a percentage of the total balance to estimate your payments.

- Credit Behavior: Lenders evaluate how reliably you’ve made payments on your student loans. Consistently paying on time builds trust, while missed or late payments could signal risk.

- Income and Financial Stability: A steady income, manageable monthly obligations and an emergency fund can help mitigate the impact of student loans on your application.

Ultimately, lenders aim to ensure you can comfortably handle monthly mortgage payments alongside your existing debts.

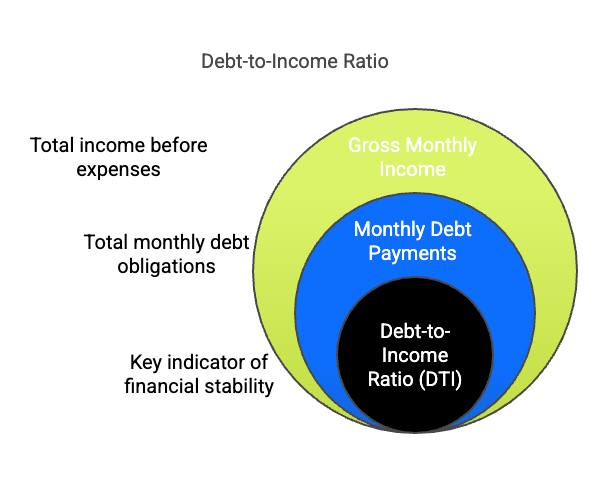

The Impact of Student Loans on Your DTI

Your DTI is a key factor lenders use to gauge your financial stability. It represents the percentage of your gross monthly income that goes toward debt payments, including student loans.

To calculate your DTI:

(Monthly Debt Payments ÷ Gross Monthly Income) × 100% = DTI (%)

For example, if your monthly debts (including student loans, credit cards and car payments) total $1,500 and your gross income is $5,000, your DTI would be:

$1,500 ÷ $5,000 × 100% = 30%

Lenders generally prefer a DTI of 36% or lower, including your anticipated mortgage payment. If your DTI exceeds this threshold, you may need to reduce debt or increase income before applying.

How Student Loans Influence Your Credit Score

Your credit score plays a significant role in determining your mortgage eligibility and interest rates. Student loans can affect your score in both positive and negative ways:

- Positive Impact: On-time payments build a strong payment history over time, which is a major component of your credit score. Student loans can also diversify your credit mix and may be your oldest account in your credit history, though the latter will benefit your score more than the former.

- Negative Impact: Late or missed payments can significantly lower your credit score and remain on your credit report for up to seven years.

Maintaining consistent, on-time payments for your student loans is one of the best ways to safeguard and improve your credit score, enhancing your mortgage prospects.

The Broader Financial Picture: DTI, Savings and Assets

Mortgage lenders also evaluate your overall financial health beyond DTI and credit score. They consider factors such as:

- Savings: A robust emergency fund and funds for a down payment show financial preparedness.

- Assets: Stocks, retirement accounts and other investments can strengthen your application by demonstrating financial stability.

- Employment History: Consistent income from stable employment is a key factor in proving your ability to repay a mortgage.

Student loans can indirectly affect these areas, particularly if they limit your ability to save. Creating a financial plan that balances student loan repayment with savings goals is crucial to achieving homeownership.

Steps to Take If You Want to Buy a Home with Student Loans

If you’re ready to pursue homeownership while managing student loans, consider these steps to strengthen your financial position:

- Evaluate Your Financial Readiness: Compare your current rent to potential mortgage payments and assess whether buying a home aligns with your long-term financial goals.

- Reduce Your DTI: Pay down high-interest debt, explore refinancing options for student loans or use income-driven repayment plans to lower your monthly obligations.

- Boost Your Credit Score: Focus on timely payments, pay down credit card balances and avoid opening new credit accounts once you decide you’ll be applying for a mortgage in the foreseeable future.

- Consider a Co-Borrower: Adding a co-borrower with strong financial credentials can lower your overall DTI and improve your chances of approval, but don’t buy more house than you can afford, even if you are approved for more than you can afford.

- Get Preapproved: A mortgage preapproval shows sellers you’re a serious buyer, which can give you an edge in negotiations and gives you a clear budget for house hunting.

Why Choose Ideal Credit Union for Your Mortgage

At Ideal Credit Union, we specialize in helping members navigate the complexities of homeownership. Our mortgage experts understand the unique challenges of managing student loans and can work with you to find solutions that fit your financial situation.

We offer:

- Competitive Rates: Get access to affordable mortgage options tailored to your needs.

- Personalized Guidance: Work with a mortgage specialist to develop a plan for improving your financial profile and achieving homeownership.

Start Your Journey to Homeownership

Your student loans don’t have to stand in the way of buying your dream home. With careful planning and the right mortgage partner, you can take control of your finances and move confidently toward homeownership.

Contact Ideal Credit Union today to speak with a mortgage advisor and explore how we can help you achieve your homeownership goals!

When you subscribe to the blog, we will send you an e-mail when there are new updates on the site so you wouldn't miss them.